Introduction

Across Central and Eastern Europe, private equity investors are reshaping the technology sector through systematic consolidation. The region has become one of the most active environments globally for buy-and-build activity, driven by a distinctive structural feature: an abundance of profitable yet highly fragmented software companies. By combining these local, founder-led or VC-backed businesses, investors are assembling scalable regional platforms. From upgrading long-standing ERP vendors in Poland to combining logistics software providers in Romania, CEE is shifting from a collection of isolated technology firms into a base for integrated, cross-border technology groups.

The technology ecosystem in the region remains unusually fragmented. Unlike the United States or Western Europe – where a small number of large incumbents dominate markets such as accounting, payroll, or logistics – CEE is characterized by strong local champions operating within narrow geographic or functional niches. Given the prevalence of small national economies, geographic consolidation is especially attractive from the perspective of American or Asian investors, as it simplifies market entry and enables access to six or seven markets at once.

In many cities from Warsaw to Bucharest, profitable software companies dominate their segment domestically but lack the capital, management capacity, or risk appetite to expand internationally.

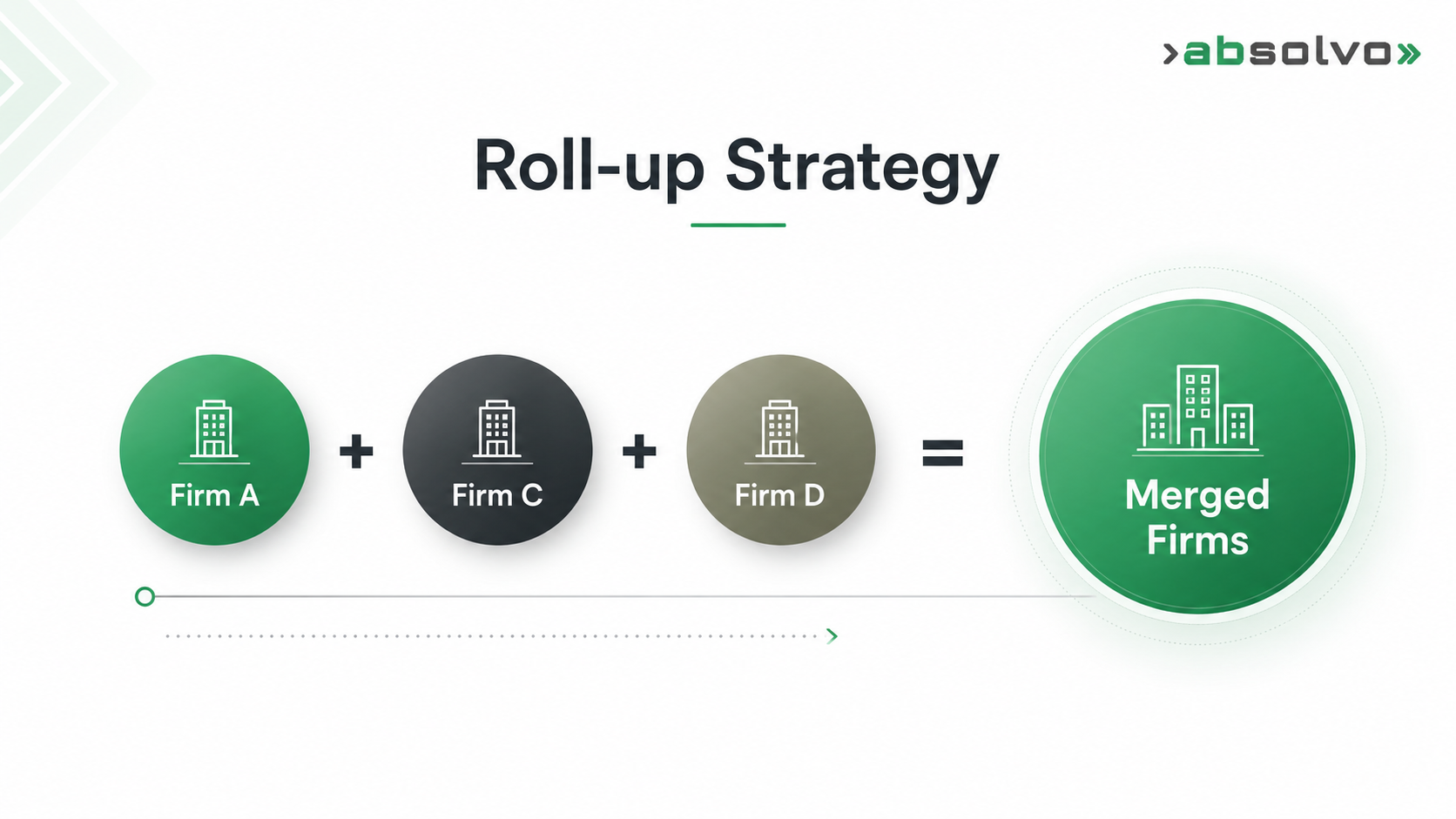

This fragmentation lends itself naturally to the "roll-up" (or "buy-and-build") strategy. In this strategy, private equity investors typically acquire one or more strong companies in a given segment and then add smaller competitors or complementary providers – known as add-ons or bolt-ons – to form a single, larger platform. In some cases, this begins with a clear market leader; in others, several similarly sized firms are merged simultaneously to create scale. This process is sometimes also referred to as a “consolidation play”. While the mechanics are straightforward, the strategic intent behind these transactions varies meaningfully, and the execution risks differ depending on the underlying objective.

In practice, most technology roll-ups in the region fall into three broad patterns.

1. Some focus on upgrading long-established software vendors whose products are deeply embedded with customers but technologically outdated.

2. Others aim to control an entire industry niche by acquiring competitors and adjacent tools across multiple countries.

3. The third group concentrates less on software products and more on people, combining IT services firms to reach the scale required to serve global enterprise clients. Distinguishing these approaches is essential, as each requires a different integration model and value-creation plan.

Modernizing entrenched software providers

One of the most common entry points for investors is the acquisition of legacy software vendors serving small and medium-sized enterprises. Across CEE, many businesses continue to rely on-premises accounting, payroll, or HR systems that are difficult to replace due to regulatory complexity and user inertia. These products generate stable cash flows but often lag technologically.

Rather than developing entirely new products, investors typically acquire the incumbent provider and use acquisitions to accelerate the transition to cloud-based delivery. A well-known example of this strategy is Symfonia in Poland. Originally the Polish division of Sage Group, the business was a mature provider of desktop accounting solutions. Following its acquisition by MidEuropa, the company embarked on a rapid shift toward a subscription-based, cloud-first model.

Instead of attempting to build cloud capabilities internally over many years, Symfonia acquired specialist firms with complementary expertise in areas such as payroll (Reset2), HR management software (HRtec) and cloud solution (Cloud Planet). This sequence of transactions transformed the company from a traditional software vendor into a broader cloud platform. The strategy was ultimately validated when MidEuropa sold a majority stake in Symfonia to Accel-KKR in 2023, demonstrating that a modernized CEE software asset could attract global technology investors at a premium valuation.

Building dominance within a single industry

Another common approach focuses less on upgrading old technology and more on controlling an entire sector. Here, investors seek to establish a central platform within a specific vertical – such as logistics, payments, or retail software – and then expand its reach by acquiring competitors and complementary products across multiple countries.

This strategy works particularly well in CEE, where specialized software providers often have strong positions in individual national markets but limited cross-border presence. By combining these businesses, investors can create platforms with both geographic reach and functional depth.

Alsendo, backed by Abris Capital, illustrates this dynamic. The group originated from Apaczka, a Polish shipping broker that helped SMEs. While profitable, the business was largely transactional. To improve scalability and margins, the investor focused on transforming it into a technology company.

They achieved this through the acquisition of Innoship, a SaaS player that managed shipping workflows for large retailers across Europe. By bolting Innoship onto Alsendo, the group didn't just gain a foothold in Romania; they added enterprise-grade shipping software and recurring-revenue characteristics, complementing the core brokerage business. This allowed them to operate a hybrid model that combines scale in shipping volumes with higher-value technology, improving margins, and strategic flexibility.

Another variation of this play is the model used by Seyfor (formerly Solitea). Backed by Sandberg Capital, Seyfor became a giant in the ERP and Point-of-Sale (POS) market not by buying one big competitor, but by acquiring over 30 smaller ones across the Czech Republic, Slovakia, and Southern Eastern Europe. They aggregated everything from restaurant checkout systems (Dotykačka) to complex HR software (Vema). By offering businesses a unified suite covering payroll, inventory, sales, and compliance, the group increased customer dependence and reduced churn. Once critical business processes are centralized with a single provider, switching costs become substantial.

A similar cross-border niche-consolidation strategy is illustrated by IAI’s acquisition of Shoprenter (advised by Absolvo), where a leading Polish e-commerce SaaS platform – backed by MCI Capital – expanded into Hungary by acquiring a strong local player with over 5,000 webshops, reinforcing its position as a regional retail-software platform rather than modernising legacy technology.

Scaling IT services through consolidation

The third strategic archetype shifts the focus from software products (SaaS) to IT Services. For decades, CEE has been a hub for nearshoring, supplying skilled developers to Western European and US clients. However, smaller development firms face structural limitations: large enterprises are reluctant to award critical projects to providers with limited scale, narrow expertise, or insufficient operational redundancy.

To overcome this barrier, investors combine multiple mid-sized IT services firms into a single organization capable of competing for large, complex contracts. The objective is not merely to increase headcount, but to broaden capabilities, diversify delivery locations, and improve credibility with global clients.

Another great example is Gloster Digital Group, now a listed company in Hungary. They executed a disciplined buy‑and‑build strategy, completing over 10 acquisitions since 2019, transforming itself from a local IT integrator into a diversified, international digital services group. The group expanded into international software development, cloud, cybersecurity, and managed services, with operations spanning four continents. What started as a hardware‑focused business is today a multi‑pillar digital platform built for scalable, cross‑border growth. Absolvo advised Gloster on many of these transactions.

Where strategies can fail

While the financial case for a CEE roll-up can look compelling on paper, execution is often far more complicated. Many buy-and-build strategies fail not because the numbers were wrong, but because integration was mishandled. In technology, unlike manufacturing or retail, the most valuable assets leave the office every evening (or log off), and the core infrastructure is frequently fragile and improvised.

In the region, investors typically encounter three operational frictions that can erode value.

1. Fragmented technology environments

Acquiring multiple small software companies means inheriting multiple technology stacks, coding practices, and databases. A common mistake is to mandate immediate standardization by forcing all businesses onto a single system right after acquisition. This approach often disrupts operations, stalls sales activity, and alienates customers.

2. Overreliance on founders

In asset-heavy businesses, ownership can change without affecting day-to-day operations. In software, the departure of a founder can undermine product direction and trigger talent loss. Many CEE founders are deeply technical and value independence, making them resistant to the reporting structures imposed by financial sponsors.

To reduce this risk, some investors redesign deal structures to keep founders engaged. Instead of a full exit, founders sell a controlling stake while retaining meaningful ownership and moving into defined leadership roles, such as overseeing product development or a specific geography. This allows them to maintain influence over technology, while the investor professionalizes functions like finance, compliance, and human resources.

3. Limited cross-border transferability

Despite the EU’s single market, B2B software – especially regulation-driven products like payroll or accounting – often struggles to scale across borders due to differing tax and labor laws. As a result, successful regional platforms localize customer- and regulator-facing elements while centralizing shared infrastructure, security, and core logic, balancing compliance with economies of scale.

Key Takeaway

To conclude, consolidation in CEE tech is no longer a distant trend, but an active force that needs to be anticipated early. It is critical to monitor whether consolidation has started in one’s relevant market, as arriving late often means facing well-capitalized, PE-backed consolidators not just as potential buyers, but as direct competitors. These platforms typically acquire aggressively, follow highly professional M&A playbooks, and therefore represent both a strategic threat and one of the most realistic exit routes.

As a result, product roadmaps, go-to-market choices, and even organizational design should increasingly be shaped with a potential PE-backed buyer in mind. In practice, founders who want to exit to such platforms often need to start positioning their businesses two to three years in advance- aligning metrics, integration of readiness, and strategic fit—rather than treating exit as a last-minute event. In a maturing CEE ecosystem, understanding where you sit in the consolidation cycle can be as important as product-market fit itself.

You might also find these interesting…

If you want to know more about different acquirers, their focus areas, ideal targets and why they are interested in the CEE region, read our deep dives on private equity and software consolidators.

Why could 2026 be a turning point for a more optimistic picture for M&A? Read more about our thorough combination of qualitative data from Absolvo’s own discussions with major global and regional strategic buyers and PE funds and latest market data translated to the CEE ecosystem.

Absolvo can support you with comprehensive exit readiness insights and the full breakdown of the key tech-exit aspects leading to a successful tech-exit masterplan. Book an appointment with our team to prepare for it together.

Absolvo can support you with comprehensive exit readiness insights and the full breakdown of the key tech-exit aspects leading to a successful tech-exit masterplan. Book an appointment with our team to prepare for it together.

.jpg)

.jpg)

.jpg)

.jpg)