Our latest stories

Breakout CEE Tech Exits: How to Sell Your Company for More Than It’s ‘Worth’

Many CEE tech company shareholders may be leaving money on the table as some exits have the potential to reach up to 2-5x fair market value. It’s not a myth; we’ve seen it happen firsthand. A big reason tech exits matter now is that many VCs who invested in 2019-2021 are facing portfolio companies that couldn’t raise a new round in 2023-2024, so the focus is shifting from “raise again” to “exit well.” In a world without free money, premiums aren’t paid for hype, or AI promises alone, especially in CEE where international expansion often delays profitability.

This dynamic is not limited to VC-backed companies. Bootstrapped founders face the same situation, and they are equally positioned to achieve premium outcomes when properly prepared. However, these outcomes are not created at the moment of exit, so founders need to start preparing early, ideally 2-3 years before launching a formal exit process. To completely understand how early preparation drives premium outcomes, we need to step back for a moment – every good story has a beginning.

And in this case, it starts in 2021, a year that felt a bit like the “gold rush” of modern M&A. Capital was cheap, interest rates were near zero, and money moved faster than ever. Ultra-low financing costs and booming equity markets created a perfect storm of aggressive spending and rapid-fire dealmaking, pushing global M&A activity to record highs.

The sobering came quickly. By 2022, global M&A value had dropped roughly 37% year-on-year, a sharp wake-up call for the entire market.

The reasons behind this 37% global M&A value drop hit from every direction:

- inflation spiked

- interest rates climbed rapidly

- financing costs surged

- bid-ask spreads widened as tech valuations fell

- geopolitical shocks rattled boardrooms

On the deal level, the cracks were just as visible:

- PE firms shifted from buying mode to repair mode

- several high-priced strategic buyers’ acquisitions from 2020-21 underperformed

- write-downs followed

- executives behind “big cheques” were put under the spotlight

- boards grew cautious on anything not supported by facts and looked like overpaying

The brakes weren’t just tapped – they were slammed. The free-money honeymoon was over, and it hasn’t returned since. Yet the story doesn’t end with a long winter.

Why the Recent M&A Upswing Could Favor CEE Tech Founders

Fast-forward three years, and as we head into 2026, that caution is still present – especially among strategic buyers who remain more selective than their financial counterparts. Still, the ice is undeniably thawing. Forecasts point to a cautiously optimistic rebound in global M&A of roughly 25% year on year, and we feel it too: buyer's appetite is picking up, dialogues are reopening, offers are improving, and momentum is gradually returning.

And when we zoom in on CEE, the picture becomes even more interesting. The talent is world-class – exceptional developers, strong engineering culture, and a vibrant innovation mindset – yet many firms still operate below the scale where valuation formulas turn generous. Years of pouring resources into product and market expansion often mean they haven’t reached the efficiency or size needed to command strong ARR multiples. And while the products themselves are impressive, many CEE tech companies struggle to fully unlock their commercial potential.

This is where the idea of a “tech exit” steps into the story. Not every company can be a market leader, and not every business reaches the level of profitability or economies of scale that trigger automatic premium valuation. In many cases, you’re not selling “amazing EBITDA” today, but the proven fundamentals and credible path to reach it. Yet CEE founders – with their talent, resilience and engineering excellence – deserve outcomes that rival those in more mature markets. To get there, however, they often need to follow a different path.

And that path does not begin when founders feel tired and decide they finally want to sell. At that point, it’s usually too late. The companies that secure the strongest valuations are the ones that start preparing long before a process officially begins – ideally 2-3 years earlier.

But how do you convince the same strategic decision-makers who got burned by overpaying 4-5 years ago to still pay a 2-3-5x premium above fair value today? Early positioning, disciplined financials, and validated synergies are among the foundational pieces that unlock premium offers. They are the difference between an average deal and a standout result in today’s CEE investment environment.

The 8 Exit Readiness Factors That Separate Breakout Deals from Average Ones

So, what does “real preparation” actually look like? We’ve distilled it into 8 critical factors that repeatedly decide whether a company lands at fair value or earns a premium. In practice, that premium isn’t negotiated with the buyer company, but with the people inside it, each with their own motivations and priorities. Want to learn what those stakeholders care about and how to navigate them? Read more here:

- Regulatory considerations: Preparing for FDI approvals and competition scrutiny is key, especially as engaging with strategic buyers early can expose sensitive information if not carefully managed but also may have impact on timing (can cause months of delay).

- IP preconditions: Clean, defensible and transferable IP in every tech deal is critical, particularly in high-barrier or fast-evolving markets where buyers place a premium on protected innovation.

- Financial structuring: Further financial deal terms matter as much as headline price, and many M&A deals include a purchase price adjustment mechanism, earn-out component or other solutions to gap valuation debates. Also, you need to decide in advance if you’re optimizing revenue growth or EBITDA.

- Stable team and contracts: A committed team with limited key-person risk and strong contractual foundations help ensure continuity and reduce post-transaction uncertainty.

- Cultural fit: Cultural alignment remains a key success factor, with 95% of executives considering it critical for smooth integration. For the founders and management this is also key: its about deciding where you and your team will belong the day after closing.

- Customer and market synergy: Clear upside potential through cross-sell; upsell and strong retention metrics can significantly enhance perceived value. Strong synergies can take the deal into different horizons.

- Pre-existing partnerships: “Try-before-you-buy” M&A, where partnerships and integrations set the stage for acquisition, paving the way for a breakout tech exit.

- Strategic alignment: Buyers are driven by different priorities, from market expansion to capability acquisition, so alignment across product, technology and strategy is essential.

If this topic has sparked your interest, you can explore deeper insights in the downloadable content on the right. Created by Absolvo’s experts, the material is designed specifically for tech founders preparing for a breakout exit.

How PE Firms Are Quietly Building CEE’s Next Tech Giants

Introduction

Across Central and Eastern Europe, private equity investors are reshaping the technology sector through systematic consolidation. The region has become one of the most active environments globally for buy-and-build activity, driven by a distinctive structural feature: an abundance of profitable yet highly fragmented software companies. By combining these local, founder-led or VC-backed businesses, investors are assembling scalable regional platforms. From upgrading long-standing ERP vendors in Poland to combining logistics software providers in Romania, CEE is shifting from a collection of isolated technology firms into a base for integrated, cross-border technology groups.

The technology ecosystem in the region remains unusually fragmented. Unlike the United States or Western Europe – where a small number of large incumbents dominate markets such as accounting, payroll, or logistics – CEE is characterized by strong local champions operating within narrow geographic or functional niches. Given the prevalence of small national economies, geographic consolidation is especially attractive from the perspective of American or Asian investors, as it simplifies market entry and enables access to six or seven markets at once.

In many cities from Warsaw to Bucharest, profitable software companies dominate their segment domestically but lack the capital, management capacity, or risk appetite to expand internationally.

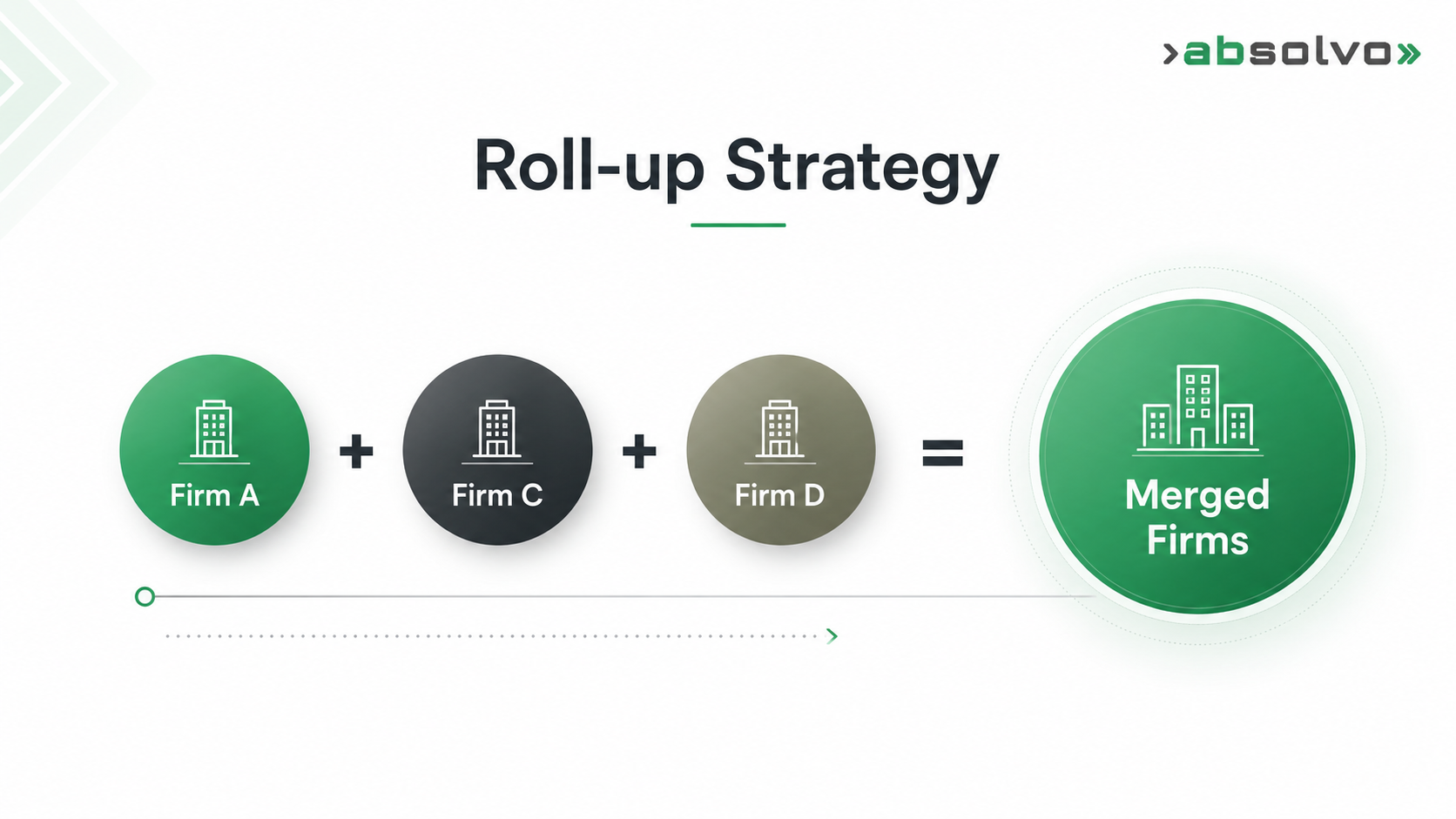

This fragmentation lends itself naturally to the "roll-up" (or "buy-and-build") strategy. In this strategy, private equity investors typically acquire one or more strong companies in a given segment and then add smaller competitors or complementary providers – known as add-ons or bolt-ons – to form a single, larger platform. In some cases, this begins with a clear market leader; in others, several similarly sized firms are merged simultaneously to create scale. This process is sometimes also referred to as a “consolidation play”. While the mechanics are straightforward, the strategic intent behind these transactions varies meaningfully, and the execution risks differ depending on the underlying objective.

In practice, most technology roll-ups in the region fall into three broad patterns.

1. Some focus on upgrading long-established software vendors whose products are deeply embedded with customers but technologically outdated.

2. Others aim to control an entire industry niche by acquiring competitors and adjacent tools across multiple countries.

3. The third group concentrates less on software products and more on people, combining IT services firms to reach the scale required to serve global enterprise clients. Distinguishing these approaches is essential, as each requires a different integration model and value-creation plan.

Modernizing entrenched software providers

One of the most common entry points for investors is the acquisition of legacy software vendors serving small and medium-sized enterprises. Across CEE, many businesses continue to rely on-premises accounting, payroll, or HR systems that are difficult to replace due to regulatory complexity and user inertia. These products generate stable cash flows but often lag technologically.

Rather than developing entirely new products, investors typically acquire the incumbent provider and use acquisitions to accelerate the transition to cloud-based delivery. A well-known example of this strategy is Symfonia in Poland. Originally the Polish division of Sage Group, the business was a mature provider of desktop accounting solutions. Following its acquisition by MidEuropa, the company embarked on a rapid shift toward a subscription-based, cloud-first model.

Instead of attempting to build cloud capabilities internally over many years, Symfonia acquired specialist firms with complementary expertise in areas such as payroll (Reset2), HR management software (HRtec) and cloud solution (Cloud Planet). This sequence of transactions transformed the company from a traditional software vendor into a broader cloud platform. The strategy was ultimately validated when MidEuropa sold a majority stake in Symfonia to Accel-KKR in 2023, demonstrating that a modernized CEE software asset could attract global technology investors at a premium valuation.

Building dominance within a single industry

Another common approach focuses less on upgrading old technology and more on controlling an entire sector. Here, investors seek to establish a central platform within a specific vertical – such as logistics, payments, or retail software – and then expand its reach by acquiring competitors and complementary products across multiple countries.

This strategy works particularly well in CEE, where specialized software providers often have strong positions in individual national markets but limited cross-border presence. By combining these businesses, investors can create platforms with both geographic reach and functional depth.

Alsendo, backed by Abris Capital, illustrates this dynamic. The group originated from Apaczka, a Polish shipping broker that helped SMEs. While profitable, the business was largely transactional. To improve scalability and margins, the investor focused on transforming it into a technology company.

They achieved this through the acquisition of Innoship, a SaaS player that managed shipping workflows for large retailers across Europe. By bolting Innoship onto Alsendo, the group didn't just gain a foothold in Romania; they added enterprise-grade shipping software and recurring-revenue characteristics, complementing the core brokerage business. This allowed them to operate a hybrid model that combines scale in shipping volumes with higher-value technology, improving margins, and strategic flexibility.

Another variation of this play is the model used by Seyfor (formerly Solitea). Backed by Sandberg Capital, Seyfor became a giant in the ERP and Point-of-Sale (POS) market not by buying one big competitor, but by acquiring over 30 smaller ones across the Czech Republic, Slovakia, and Southern Eastern Europe. They aggregated everything from restaurant checkout systems (Dotykačka) to complex HR software (Vema). By offering businesses a unified suite covering payroll, inventory, sales, and compliance, the group increased customer dependence and reduced churn. Once critical business processes are centralized with a single provider, switching costs become substantial.

A similar cross-border niche-consolidation strategy is illustrated by IAI’s acquisition of Shoprenter (advised by Absolvo), where a leading Polish e-commerce SaaS platform – backed by MCI Capital – expanded into Hungary by acquiring a strong local player with over 5,000 webshops, reinforcing its position as a regional retail-software platform rather than modernising legacy technology.

Scaling IT services through consolidation

The third strategic archetype shifts the focus from software products (SaaS) to IT Services. For decades, CEE has been a hub for nearshoring, supplying skilled developers to Western European and US clients. However, smaller development firms face structural limitations: large enterprises are reluctant to award critical projects to providers with limited scale, narrow expertise, or insufficient operational redundancy.

To overcome this barrier, investors combine multiple mid-sized IT services firms into a single organization capable of competing for large, complex contracts. The objective is not merely to increase headcount, but to broaden capabilities, diversify delivery locations, and improve credibility with global clients.

Another great example is Gloster Digital Group, now a listed company in Hungary. They executed a disciplined buy‑and‑build strategy, completing over 10 acquisitions since 2019, transforming itself from a local IT integrator into a diversified, international digital services group. The group expanded into international software development, cloud, cybersecurity, and managed services, with operations spanning four continents. What started as a hardware‑focused business is today a multi‑pillar digital platform built for scalable, cross‑border growth. Absolvo advised Gloster on many of these transactions.

Where strategies can fail

While the financial case for a CEE roll-up can look compelling on paper, execution is often far more complicated. Many buy-and-build strategies fail not because the numbers were wrong, but because integration was mishandled. In technology, unlike manufacturing or retail, the most valuable assets leave the office every evening (or log off), and the core infrastructure is frequently fragile and improvised.

In the region, investors typically encounter three operational frictions that can erode value.

1. Fragmented technology environments

Acquiring multiple small software companies means inheriting multiple technology stacks, coding practices, and databases. A common mistake is to mandate immediate standardization by forcing all businesses onto a single system right after acquisition. This approach often disrupts operations, stalls sales activity, and alienates customers.

2. Overreliance on founders

In asset-heavy businesses, ownership can change without affecting day-to-day operations. In software, the departure of a founder can undermine product direction and trigger talent loss. Many CEE founders are deeply technical and value independence, making them resistant to the reporting structures imposed by financial sponsors.

To reduce this risk, some investors redesign deal structures to keep founders engaged. Instead of a full exit, founders sell a controlling stake while retaining meaningful ownership and moving into defined leadership roles, such as overseeing product development or a specific geography. This allows them to maintain influence over technology, while the investor professionalizes functions like finance, compliance, and human resources.

3. Limited cross-border transferability

Despite the EU’s single market, B2B software – especially regulation-driven products like payroll or accounting – often struggles to scale across borders due to differing tax and labor laws. As a result, successful regional platforms localize customer- and regulator-facing elements while centralizing shared infrastructure, security, and core logic, balancing compliance with economies of scale.

Key Takeaway

To conclude, consolidation in CEE tech is no longer a distant trend, but an active force that needs to be anticipated early. It is critical to monitor whether consolidation has started in one’s relevant market, as arriving late often means facing well-capitalized, PE-backed consolidators not just as potential buyers, but as direct competitors. These platforms typically acquire aggressively, follow highly professional M&A playbooks, and therefore represent both a strategic threat and one of the most realistic exit routes.

As a result, product roadmaps, go-to-market choices, and even organizational design should increasingly be shaped with a potential PE-backed buyer in mind. In practice, founders who want to exit to such platforms often need to start positioning their businesses two to three years in advance- aligning metrics, integration of readiness, and strategic fit—rather than treating exit as a last-minute event. In a maturing CEE ecosystem, understanding where you sit in the consolidation cycle can be as important as product-market fit itself.

Venture Capital in general and in CEE – Key Insights for Businesses that want to boost their growth with fresh funding (Part 2)

What Are VCs Looking For?

Below are the most important factors that venture capital investors consider when evaluating an investment opportunity and making decisions. These aspects can also help you determine if your business is ready to raise capital.

• Growth Potential of the Industry and Large Market Size

Venture capital investors typically expect robust growth, which is usually achievable only in thriving industries. Facing many well-capitalized competitors that started earlier can reduce your chances. The industry must have some entry barriers to prevent new competitors from easily replicating your solution. A key factor is whether the market is large enough (TAM – Total Addressable Market). A small market limits the possibility of substantial growth, which will also restrict the exit options.

• Outstanding Growth Potential

You need a growth strategy and a well-founded, bottom-up business plan for the next 4–5 years, convincingly demonstrating to investors that the investment can achieve the expected returns (e.g., 5–10-20-50x). Identifying and analyzing risks and presenting plans to mitigate them are crucial parts of this strategy.

• Proven Market Demand and Business Model, Traction

Depending on the stage and maturity of your business, you must show different levels of “proof.” At a minimum, you need evidence and initial market feedback validating your concept. In concrete terms, you should have initial customers and sales or at least one or two pilot projects to demonstrate that your concept works and customers are willing to pay for it. If you're seeking funding for international expansion, investors will expect knowledge of the target markets, a team member capable of managing this expansion, and ideally some initial results in those markets. Being a market leader makes this process significantly easier.

• Unique Competitive Advantage, USP

A clearly defined USP (unique selling proposition) or competitive advantage is a prerequisite for a successful business and venture capital investment. The competitive advantage must be real and distinguishable—generic claims like “fast,” “efficient,” or “flexible” won’t suffice. A price advantage alone is not valuable. Furthermore, the competitive advantage must be defensible and at least sustainable in the medium term.

• Exceptional, Competent Team with a Credible Track Record

One of the core principles of venture capital is that investors bet on the jockey, not the horse. The management team is scrutinized closely, and attributes like leadership experience, prior professional achievements, and commitment are essential. For early-stage venture capital investments, the quality, composition, and dynamics of the team are often decisive factors. Investors are more likely to invest in an excellent team with an average idea than in an average team with an excellent idea because the team is what drives success.

• Scalability and International Perspective

Due to their high return expectations, venture capital investors rarely believe local CEE companies can achieve the desired growth solely in their domestic market. At least a regional, ideally global model is required. When planning expansion, carefully consider which target countries to enter, why, and how you’ll serve local customers. Other business models allow you to be born global from day one. You should not optimize for the local market, for the local customer needs. A standard Series A investment typically requires a proven, scalable acquisition channel supported by data to demonstrate that a robust system exists. For example, if €1 million is injected into the business, investors should have a clear idea of how many customers and how much revenue this will generate.

• Attractive Exit Opportunity Within ~5 Years

As mentioned earlier, venture capital is inherently exit-oriented, aiming to realize returns within 4–5 years. A business ready for this “marriage” shall have a developed exit strategy (not required in very early stage). You should showcase current M&A transactions in the industry and future potential targets, explaining why your business could become an acquisition target in a few years and identifying potential buyers.

• Soft Parameters

These include all non-quantifiable factors, such as personal impressions, feelings, and “chemistry,” which can influence the investor’s decision and, in extreme cases, even derail a transaction. Remember, venture capital investment ties both parties together for years, so mutual impressions matter. Does the other party arrive punctually for meetings? Do they take long vacations? How do they behave during informal conversations? Even seemingly trivial details—such as how you ask for coffee from the assistant —can impact an investor's perception. It’s surprising how many small things can influence an investor!

How to Prepare Before Approaching VC Investors?

The further a startup progresses on its own (i.e bootstrapping) in the implementation process, the more likely it is to capture the interest of one (or even multiple) investors. It’s rare for an investor to provide hundreds of millions of euros to finence an early-stage project still in the idea phase. This isn’t due to doubts about innovation or growth but rather the risk factors associated with early-stage ventures. Some say: Ideas are nothing, execution is key.

Once a prototype is truly functional, embraced by the market, and has achieved market traction or even a leading position, the risk decreases significantly. At that point, investors are much more willing to provide substantial funding.

It’s critical to assess how to advance your project further before approaching investors. This might include validating realistic market demand and presenting needs as accurately as possible.

For businesses that have been successfully operating for several years, thorough planning of the growth strategy and establishing a clear roadmap can support investment decisions. Every company wants to close its deal as quickly as possible. Investors want to understand what’s the story they’re investing and how they’ll get returns—there will be questions! Be proactive and prepare a business plan based on metrics ad benchmarks, covering market research findings, competitor analysis, core strategy elements, sales and marketing channels, and more.

Before reaching out to investors, you should have:

- A detailed investor presentation,

- A shorter pitch deck

- Competition analysis and summary of market research and trends

- TAM estimation

- And a business plan - at the very least

What Questions Can You Expect When Approaching Investors?

If you plan to grow further with the involvement of venture capital investors, you’ll need to provide convincing answers to questions like:

- What makes your product/solution unique, and how does it stand out from competitors?

- What are the most important market trends influencing your success?

- What regulatory challenges or risks might you face?

- Is your intellectual property protected? If not, should it be, and when?

- Which country is best to launch in first, and why?

- What market players should you expect there, and what level of demand can you anticipate?

- What is the market size (TAM)?

- What are the expected customer acquisition costs (CAC), customer lifetime value (CLV), and sales conversion rates?

- Would a joint venture, a reseller network or a local office be the better solution for you?

- What costs and returns are associated with each option?

- How will your gross margin evolve throughout the years?

- What makes your offering/solution sticky?

- Can you utilize network affects? How?

- What costs and returns are associated with each option?

- Can the business deliver above-average returns as expected by investors?

- Do you have an idea about the investor’s exit? What exit value would satisfy you?

This list is far from exhaustive. However, thorough preparation can significantly enhance the credibility of your project, increasing the likelihood of a successful fundraising process!

How Long Does It Take to Find an Investor?

Each project and investor are unique, making it challenging to estimate the time required to find the right investor. Extreme cases do exist—some companies have secured investors in just a few weeks, while others have taken more than a year. Realistically, for raising venture capital , you should plan for a process lasting 6–12 months.

The more progress you make independently (collecting feedback from the market, implementing plans beyond the concept stage, entering international markets, gathering experience, etc.), the shorter the average investment timeline can be. Involving experts can also streamline and accelerate the process. Several years of expertise and experience like Absolvo’s can significantly reduce the required preparation time.

What Does the Capital Raising Process Look Like?

You can read more about the main phases of the process here >>

The Typical Conditions of VC Investment

The details of the specific collaboration are outlined in the investor's offer (indicative offer, LOI, NBO), known as the term sheet. It is unique to each project, company, and investment.

Some parts of the term sheet are standard, but many terms are negotiable - and they should be negotiated well! Whether an investor's offer is advantageous is not solely and primarily determined by the ownership stake requested or the company valuation

- contrary to what many founders or owners might initially believe. The term sheet contains numerous additional conditions that can significantly influence the overall picture, potentially even changing the perception of the offer entirely.

For most businesses, capital raising is not an everyday task, so it's completely natural that interpreting a term sheet, evaluating its conditions, and negotiating them aren't routine activities either.

Experts in capital raising can support businesses also in this area. Up-to-date expertise, knowledge of truly "standard" conditions, experience with investors, and years of professional negotiation, and transaction experience increase the likelihood of achieving a genuinely "good deal". A poorly negotiated agreement can lock both parties into years of disadvantageous and demotivating "co-suffering" instead of a fruitful collaboration.

Just to mention a few topics:

During negotiations, can we expect the investor to waive their drag-along rights? Should we fully accept their veto rights? How should we address an early exit? What can we expect regarding liquidation preferences. Will we even receive cash at the time of exit? Is a right of first refusal key for the founders? What happens if the company needs further financing? Who should be on the board? What are the relevant reserved matters for the board and/or the shareholders meeting?

So, it is beneficial to:

- discuss these questions with an experienced advisor and prepare with their guidance.

- understand the chosen investor's preferences in advance and prepare strategically.

- have an experienced team evaluate the offer provided by the investor.

How Do You Increase Your Chances with International Investors?

- It's not enough to be good; you must demonstrate competitive advantage and a unique selling proposition (USP) on an international level.

- Your revenue likely doesn’t come solely from the domestic market anymore, proving your ability to succeed in international business development and customer acquisition.

- Your team must be capable of building an international company, ideally including foreign team members.

- You plan to establish a presence in your target market (e.g., opening an office or even relocating a founder), or even better, this process is already underway.

A common pattern is that founders have lived or worked abroad, attended foreign universities, or participated in non-local accelerator programs - showing that their ability to succeed in a foreign culture and build a successful business won’t be tested using the investor’s money.

When Is Venture Capital Not the Right Fit for You?

- If during the planning phase, it becomes evident that the project or company cannot achieve annual growth of at least 30-50% (of course depending on the basis).

- If market analysis reveals that your competitive advantage is only temporarily sustainable.

- If the market is not large enough (TAM shall be above €500Mn or even 1Bn).

- If you're not willing to sell the company after 3-5-7 years.

In these cases, it’s worth reconsidering whether your idea or plan can deliver the return investors expect. As previously mentioned, securing venture capital investment is a lengthy, time-consuming process requiring significant energy.

Additionally, Avoid Seeking Investors if:

- You need external funding immediately, as the minimum expected six-month capital raising process length is a "slow solution for you."

- If you struggle with the idea of accepting investors as co-owners, feel reluctant to give up equity—even temporarily—or allow them a say in company decisions. Getting VC money inherently means the investor will become a co-owner for a specific period, so you should be onboard with that from the beginning.

- You disagree that planning growth, developing strategies, and preparing business calculations are indispensable for securing a partner or funding for your project. These strategy-related questions will undoubtedly be asked.

Venture Capital in general and in CEE – Key Insights for Businesses that want to boost their growth with fresh funding (Part 1)

While venture capital offers opportunities to accelerate expansion, growth, the process of securing VC investment is complex. It requires an understanding of investor expectations, proper planning of strategy and financials; detailed term sheet and investment agreement negotiations.

Venture capital (VC) is an equity-based financing method, typically used by businesses with high growth potential in specific phases of their lifecycle—particularly in early and growth stages.

The financing needs and options for companies vary significantly depending on whether they are in an early- or a more mature growth phase.

Early-stage businesses require different types of funding compared to well-established companies. As businesses mature, other financing sources often take precedence, such as private equity, strategic investors, or stock market listings. Each stage comes with unique challenges, tasks, risk factors, and growth objectives.

In both regional and international practice, venture capital investors (those who you meet are GPs, or general partners) are managing venture capital funds. These funds are financed by institutional investors (e.g. banks, international financial organizations, investment funds, insurers) and high-net-worth individuals – they are the LPs or limited partners.

A CEE regional characteristic is that funds rely heavily on government or EU resources, which influence both the available investment opportunities and the applicable rules.

Venture capital investors primarily target companies (startups) with exceptional talent and growth potential, often at early stages, but with higher risks. They invest in partnership with the founders in exchange for equity (shares, stakes), becoming co-owners of your business, so this is not a loan or grant!

In return for taking higher risks, venture capital investors expect above-average returns. Depending on the fund manager, they typically aim for a return on investment of 3-10-times. For example, if they invest €1 million, they expect to receive €3–5–10 million in return.

Venture capital investors typically invest for a period of 4–5 years, after which they exit the investment by selling their stake. This exit can occur in various ways: they may sell their shares back to the founders or existing owners (more common with state-backed funds), but most often, they sell to a third party, typically a strategic investor (trade sale) or another financial investor, such as private equity funds.

The return on the investment is realized at the time of exit—when the company is sold—so there is no requirement to pay monthly or annual interest or principal. Venture capitalists aim to achieve their return during the exit phase and are, therefore, motivated to drive significant value creation and company growth in the meantime.

The Risk-Reward Dynamic of Venture Capital Funds

Companies that raise venture capital are referred to as portfolio companies, as funds typically manage multiple investments simultaneously, forming a portfolio. As being financial investors, their primary goal—and the expectation of their investors—is to manage the overall portfolio’s returns while mitigating risks at the portfolio level.

Some portfolio companies may only partially achieve the expected return by the end of the investment period, or not at all, while others may exceed expectations, achieving significant growth and a successful exit. These high-performing companies can offset the underperforming or failed investments.

VCs know not every investment will make returns, and some may even result in losses. This risk-reward dynamic explains why

venture capitalists seek such high returns on each deal. While they typically do not involve themselves in daily operations, they actively engage in strategic and major financial decisions affecting the business and its profitability (e.g. loan decisions, large CAPEX items etc.).

Fund managers are inherently interested in supporting the growth of portfolio companies, as their personal return (through so-called carry) is connected to the exit value which depends on how much the company has grown.

Venture Capital and Other Equity Financing Options by Growth Stage

Once the need for capital raise is identified, the most critical step is to clarify the type of investor that fits—which depends on the current growth stage of the business and the goals it seeks to achieve with investment.

Depending on whether your business is in its early stages or a more mature phase, it’s important to approach the most suitable type of investor. Across the CEE region, there are numerous opportunities for companies with innovative business solutions, unfair competitive advantages, and strong market potential to secure fresh capital for growth, expansion, and transitioning to the next stage of maturity.

Matching your expected results and objectives with the right investor pool is a critical step in the capital raising process.

Businesses at different maturity stages can access the following primary types of equity financing sources:

- Early-stage companies can secure funding from angel investors or seed-stage VCs, typically in the range of EUR 50,000–300,000 in the CEE region. Some seed or late-seed deals nowadays are rather in EUR 1-3 million range.

- Growth-stage companies operating in innovative sectors, with developed products that are already on the market, proven market feedback, and significant international revenues, can consider growth capital investments from venture capital funds. These investments range in the CEE from EUR 4–10 million. You’ll see “Series A / B / C” rounds, referring to the first, second etc rounds and possible share class.

- Well-established companies, even in traditional industries, that are operating successfully with revenues in the ten. millions of EUR, a strong market position, and generating significant EBITDA, may require external capital to accelerate growth and expansion, acquire other players or competitors, restructure debt, buy out a co-owner, or improve operations. These companies are typically suited for private equity funds or, in specific cases, turnaround funds.

- Buyouts are usually executed by strategic investors or private equity funds, though fresh capital in the form of equity injections is also an option, from even EUR 1-5 million, however a typical CEE PE fund will look for deals above 10-20 million.

Venture Capital or Bank Loans?

For more mature businesses with several years of operational history and historical performance data, bank loans can be a viable solution for financing investment plans, provided they can offer sufficient collateral. However, for early-stage companies with limited collateral and seeking financing several times their revenue to support growth, scaling, or international expansion, venture capital may be a more viable option.

Venture capital is a specialized form of financing where bank loans are not really alternatives.

Key Differences Between Venture Capital and Bank Loans

- Repayment structure: One of the most significant differences is the repayment method. Bank loans require fixed repayments with interest, typically sourced from the company’s cash flow, regardless of its profitability or success. Venture capital investors, by contrast, realize their return at the end of the 3–5-year investment period during the exit phase. This means no cash is drained from the company for repayment during the investment period.

- Ownership approach: Unlike lenders, venture capital investors view themselves as co-owners and business partners, committed to driving the company’s growth. Banks, on the other hand, are not invested in the company’s success and do not participate (nor have the expertise to participate) in its operations.

- Added value: Venture capital can provide significant momentum for a company, as investors often contribute more than just capital. They can offer industry knowledge, strategic guidance, and access to networks (known as "smart money") to help the company achieve higher value creation and return on investment.

Types, Key Characteristics, and Volume of Venture Capital and Private Equity Investments

The types, main characteristics, objectives, and volumes of venture capital and private equity investments can be summarized as follows:

What’s next?

How can you identify the potential investors to approach in the first round? How many can you negotiate with parallel? How will you learn about the investors’ backgrounds and preferences before your first meeting? What advantages and synergies can you present to them?

Read Part 2 here >>

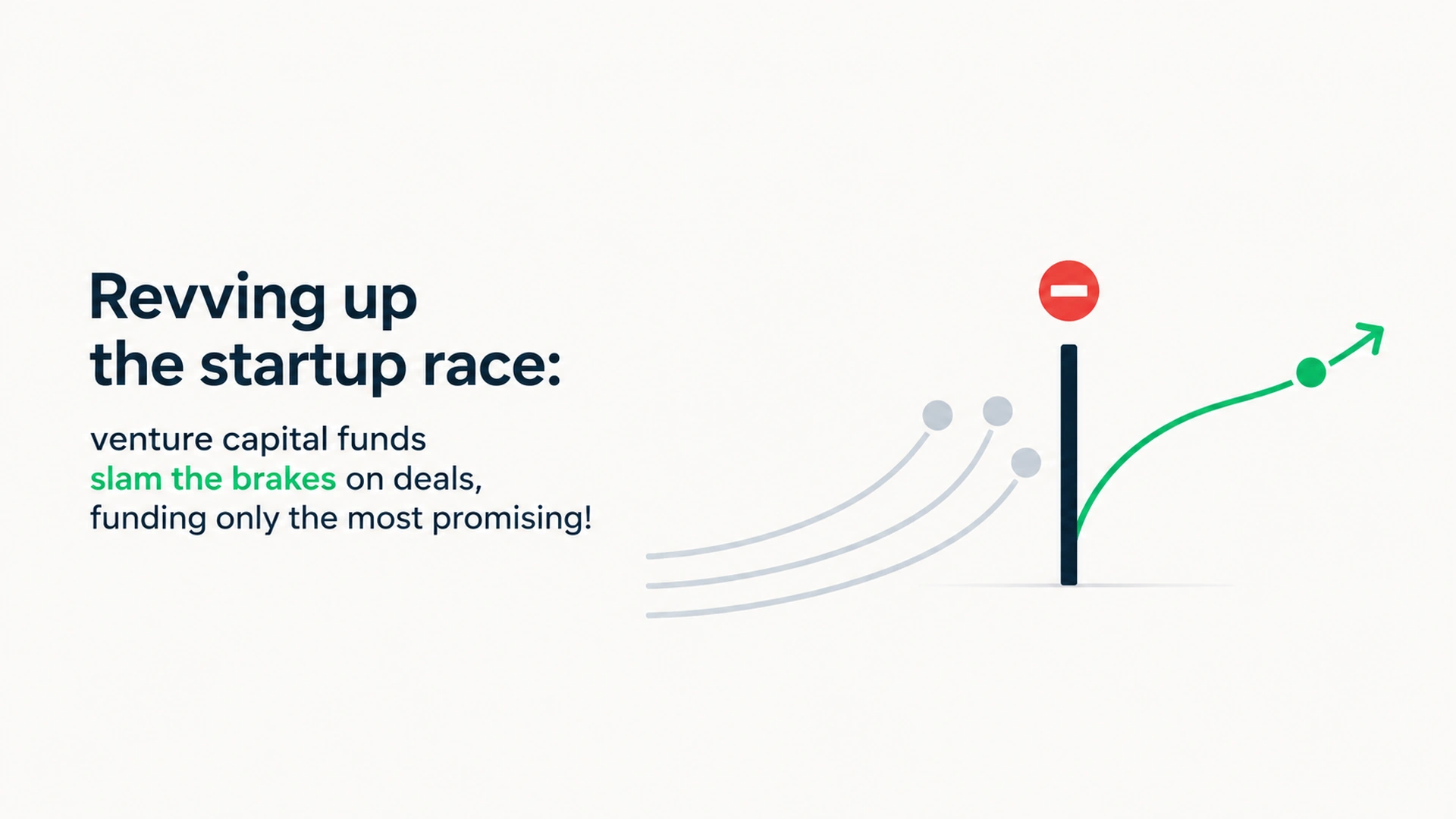

Revving up the startup race: venture capital funds slam the brakes on deals, funding only the most promising!

VC funds slam the brake on deals

VC firms are becoming increasingly discerning, carefully selecting only the most promising and deserving startups to support. This change reflects a growing emphasis on quality over quantity, as funds concentrate their resources on backing the truly exceptional companies that have the potential to make a lasting impact in the market.

The current fiscal year has witnessed a notable downturn in the completion of venture capital deals, marking a considerable departure from the upward trajectory observed since 2016. This extraordinary reduction in the volume of completed transactions, when evaluated in the context of the past decade, highlights a momentous shift in the market dynamics. Nevertheless, it is crucial to contextualize this development, as comparable trends have emerged across both Western European and American markets.

While the magnitude of the decline may appear alarming, a broader perspective reveals a more nuanced picture of the prevailing landscape. However, one thing remains certain: the startup race is revving up in 2023 and only the most promising contenders will secure the fuel they need to accelerate towards success.

Growth trends – number of tech deals over the past years

Over the past years, the Central and Eastern European (CEE) region has exhibited a consistent and robust growth trend. As evidenced by the accompanying table, this growth trajectory has been remarkable and sustained, extending until the first half of 2022, with positive year-on-year growth figures recorded from the second half of 2017 until H2 of 2022. It is worth highlighting that the CEE region’s growth rate has demonstrated resilience amidst the challenges presented by the COVID-19 pandemic in 2020, setting it apart from the tech venture capital markets in Western Europe and the USA, which experienced a slight decline during this period. Moreover, it is noteworthy that even prior to the pandemic, the tech venture capital markets in Western Europe and the USA exhibited a slower rate of increase when compared to the thriving CEE venture capital market.

The COVID-19 pandemic, however, proved to be a notable turning point in the trajectory of recent trends, particularly within the CEE venture capital market. Following a period of significant growth, the pace of expansion began to be moderate, contrasting with the Western European and US markets which experienced a remarkable resurgence, with the US market achieving an impressive 31% growth rate within a year. Subsequently, all three markets experienced a considerable slowdown, culminating in a decline six months later. Notably, in 2023, the CEE market experienced the most pronounced downturn following its previous period of robust growth, with only a fraction of the deals being completed compared to the previous year.

The impact of downturn across all stages of VC cycle

The downturn has inevitably impacted all stages of the venture capital cycle. However, it is important to note that the severity of the impact varied across different stages. As depicted in the graph below, it becomes evident that venture capital firms are not really experiencing a shortage of funds. Rather, they have adopted a more discerning approach, exercised caution and carefully evaluating investment opportunities in startups. Consequently, the later stage, which typically requires a significant infusion of capital, experienced a relatively lesser decline compared to earlier stages.

Venture capital firms are adopting a more selective approach, prioritizing investments that exhibit strong growth potential, sustainable business models, and a clear path to profitability.

Implications on capital investments and average deal sizes

Following an analysis of the volume of successfully closed transactions, it is now imperative to address the implications of the venture capital market downturn on capital investment. The presented graphs indicate a gradual return to pre-COVID levels of capital investment in both Western Europe and the CEE region. Nevertheless, it is important to acknowledge that the extraordinary growth observed in 2021 and 2022 is unlikely to be replicated. As such, the market is now undergoing a process of normalization, marking a transition from the extraordinary highs observed in the previous years.

When considering investments across different stages, there are slight differences between Western Europe and the CEE region. In Western Europe, a unanimous peak was observed in 2021, followed by a gradual and subsequently rapid decline, except for the seed and later stages. Conversely, the CEE region exhibits a less predictable and stable pattern.

The provided tables reinforce the notion that VC firms are not experiencing a shortage of capital, albeit accompanied by a decline in the number of investments. This assertion is supported by the sustained value levels observed in early-stage investments in the CEE region, while angel and accelerator investments didn’t experience notable decreases either. It is worth noting that although later stage investments also declined, such figures can be disproportionately influenced by one or two outliers characterized by exceptionally high investment amounts. In contrast, preceding stages exhibit a more substantial sample size of deals, with fewer extreme values.

So, what key insights and strategic approaches should startups be aware of considering the current circumstances?

- Firstly, they should be prepared for an extended timeline in securing funding. Building and nurturing relationships, as well as leveraging networks, have become increasingly valuable assets in the fundraising process. Startups must prioritize cultivating strong connections with potential investors, industry experts, and strategic partners to enhance their credibility and access to funding opportunities.

- Furthermore, it is crucial for them to be proactive in managing their financial situation. If a startup finds itself in dire need of funding, they should be prepared for the possibility of a downround, wherein the valuation of the company may be lower than previous investment rounds. To mitigate this risk, startups should focus on preserving cash, extending their financial runway, and pursuing organic growth opportunities.

- In this competitive landscape, startups should also reassess their market strategy. It is essential to not only survive but also outperform competitors. By effectively positioning themselves in the market, startups can attract and retain customers, thereby gaining a competitive advantage and potentially expanding their market share.

About Absolvo

Absolvo provides end-to-end M&A and Growth Capital advisory support for tech or innovation-focused companies, visionary entrepreneurs and investors. We support our clients who are about to raise capital, seek acquisition targets, sell their business, or plan an exit. With over €3.4 billion in closed deals, deep industry expertise, regional market knowledge, and data-driven insights gained from 500+ projects, our team helps turn even the most complex deals into reality and success.